AI trading collapses? Bond Market "Knocks Out" the Stock Market

Cracks in the bond market are turning into earthquakes for the stock market.

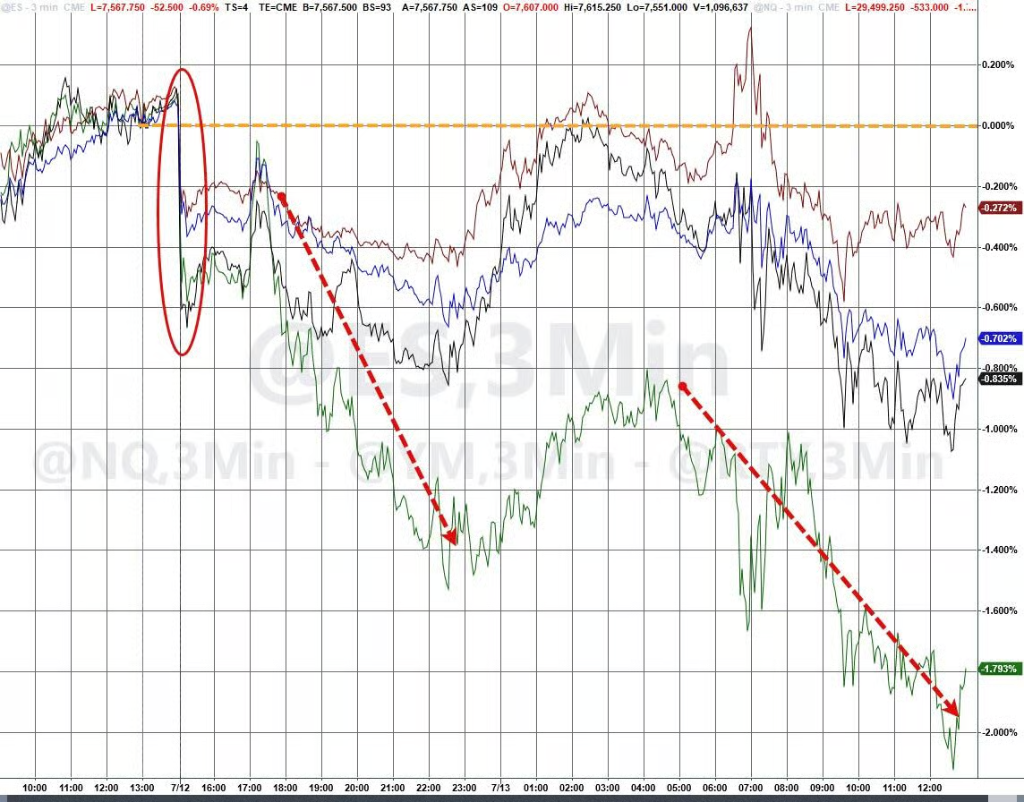

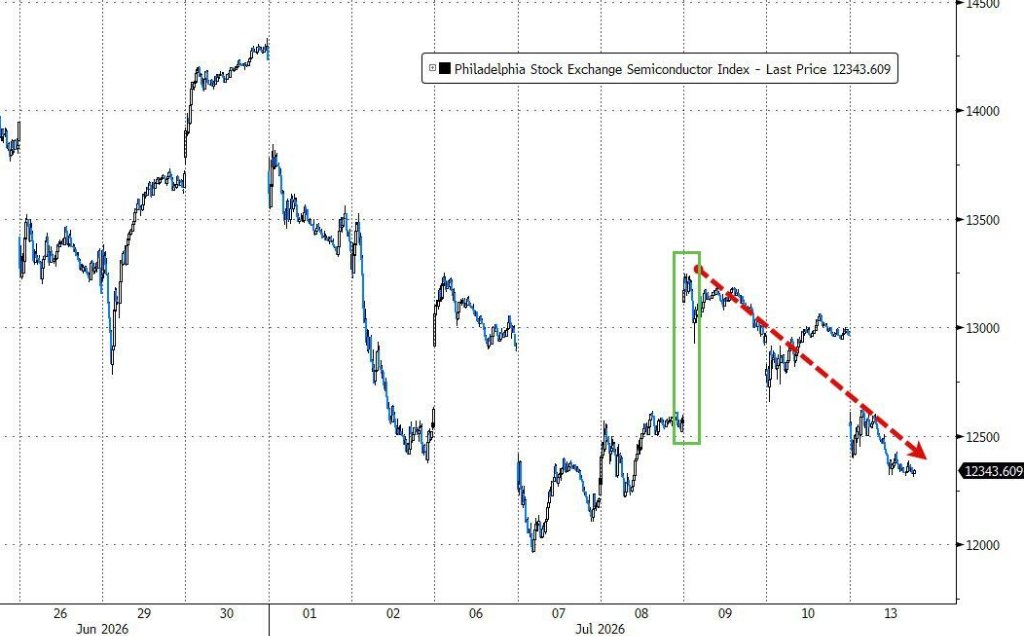

On July 13 local time, US semiconductor stocks were "knocked down," and the entire AI sector collapsed. Following a brutal near 9% drop in South Korea's KOSPI index, the Nasdaq once again fell below its 50-day moving average and closed below it, making it the worst-performing of the major US stock indices that day.

The semiconductor sector was hit hard, and AI-related stocks were sold off across the board—both the "issuers" (those investing in capital expenditure, such as cloud computing giants) and the "receivers" (those providing computing power, like chip companies) were not spared, with the latter suffering deeper declines.

Interestingly, the Mag7 and the remaining 493 stocks in the S&P saw nearly the same level of decline that day—this indicates that it's not merely a style rotation, but a broader contraction in market sentiment.

On this day, three main trading narratives tightened simultaneously: US-Iran tensions pushed up oil prices, hawkish comments from the Federal Reserve crushed the bond market, and the debt risks of AI capital expenditure triggered a sell-off in the semiconductor sector. However, the "brutality" in the bond market may actually be one of the core warning signals truly worth noting.

The logic chain of AI trading is: Tech giants issue debt → invest heavily in building data centers → drive up demand for computing power → semiconductor and AI stocks rally. Now, the very first link in this chain—the bond market's capacity to absorb new debt—is weakening. Brian Garrett, Goldman Sachs' head of derivatives trading, bluntly said this week: "This is the first time in years that my credit colleagues are more nervous than the equity volatility team... the word 'brutality' has been repeated over and over at the credit trading desk, while the S&P 500's volatility over the same period has swung in a range of only 30 basis points."

Bond Market Alert: AI Borrowing Frenzy Hits Absorption Limits

The scale of AI-related bond issuance has pushed the investment-grade bond market to the verge of indigestion.

According to The Wall Street Journal, six hyperscale computing companies—Alphabet, Amazon, Meta, Oracle, Nvidia, and SpaceX—have already issued about $244 billion in bonds so far this year, more than double last year's total of $108 billion, and over 14 times the $17 billion in 2024.

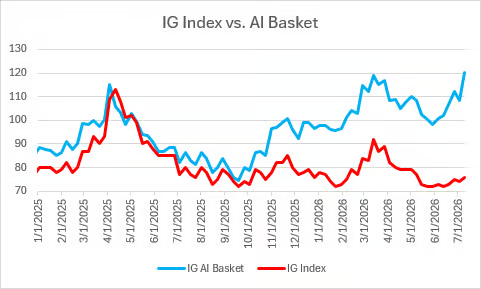

Goldman Sachs investment-grade bond trader Jeffrey Papai wrote in a report: "In the past month alone, AI-related bond issuance has reached $75 billion (year-to-date $241 billion, $360 billion over the past year), causing spreads in our AI bond basket to widen by about 25 basis points."

More importantly, the market's absorption threshold is dropping rapidly. Papai noted: "Previously, it took over $75 billion in supply to stress the market; now, just $25 billion is enough to put the market on the defensive." In other words, the market is less and less able to withstand the same shocks.

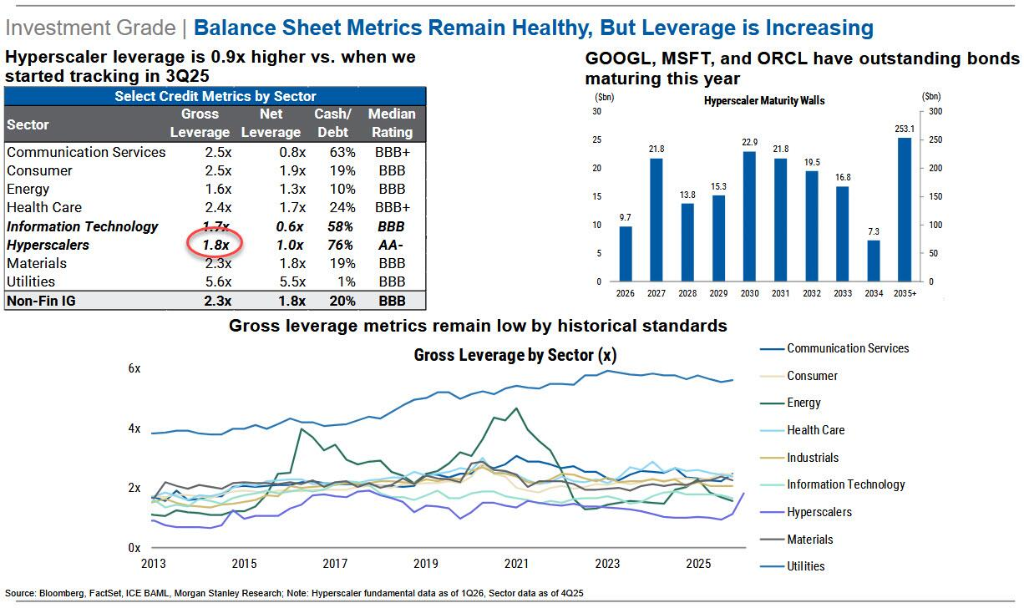

According to Morgan Stanley, the overall leverage ratio of hyperscale computing firms has soared from 0.9x in Q3 2025 to 1.8x now, doubling in just over two quarters—surpassing the leverage of the entire energy sector, and still climbing at about 0.3x per quarter.

From a market share perspective, Amazon, Meta, Google, Microsoft, and Oracle now account for 4% of the entire US dollar investment-grade bond index. By DV01 (duration weighted) measure, the six hyperscale computing firms plus three major chip companies now represent 9% of the index—and that's before chip funding has truly begun.

Papai's conclusion is straightforward: "It is clear from recent market moves that incremental absorption capacity from investors has shrunk dramatically."

Why does trouble in the bond market drag down the stock market too?

The logic is direct: AI capital expenditure is supported by debt, and debt needs to be bought by investors.

Papai admits that digesting the next round of supply requires several preconditions: issuers should slow the pace, change issuance structure (diversifying currencies and maturities), private credit and banks should absorb more, and bond prices should further decline (wider spreads) to attract new buyers.

But he also highlights the inner contradiction of this path:

Should an AI bond sell-off unfold, it would directly shock the equity market and could spread to the broader investment-grade space.

Michael Hartnett, Chief Investment Strategist at Bank of America, lists "AI capital expenditure cuts" as the biggest tail risk for the market and gives a trigger path: bond vigilantes cut off liquidity to hyperscale computing companies, forcing them to shift to equity financing and lay off employees—Meta, Microsoft, and Amazon have already cut their staff by 13%, 10%, and 9% respectively.

Apollo's chief economist, Torsten Slok, warns:

AI is currently the only pillar supporting the economy and markets. With so many bets on so few companies, if the payoff comes later than expected, this is not just an industry issue—it could tip the economy into recession and pull the S&P 500 into a correction.

Slok also points out that token prices continue to fall, and Chinese models have surpassed their US peers in both share and token usage among the world's most-used models—further compressing the free cash flow outlook for hyperscale computing companies.

Can this round of narrative be "revived" again?

This isn't the first time the AI bond market has approached a critical point.

In early May 2026, the Financial Times reported that J.P. Morgan, Morgan Stanley, and SMBC were looking to shift data center-related debt risk to a wider pool of investors, as core buyers have grown wary of AI bond supply.

At that time, Goldman Sachs published its "Decoding the Agent Economy" report within about 48 hours of the article's release, predicting that agent AI would drive substantial increases in LLM profit margins. The narrative shift quickly calmed market nerves and spurred another much larger wave of bond issuance—Amazon completed a $37 billion issue in March (the fourth largest in history) and another $25 billion in July; SpaceX tapped the market with a $25 billion bond sale just days after its IPO.

Now, with the Goldman credit desk itself calling conditions "brutal," it signals that the strength of this narrative's support is waning.

Papai wrote in the report:

Given that spreads have already adjusted and the issuance window is nearing the earnings blackout period, AI bonds may get a short-term reprieve, but over the medium-to-long term, given the expected supply, they are likely to underperform the market further. We recommend holding credit volatility positions to hedge the risk of broader market 'contagion'.

Beyond the bond market: Waller’s Rate Hike Warning + Oil Price Shock

On this day, bond market pressure also came from another direction.

Fed Governor Waller’s speech in New York directly fueled rate hike expectations:

If this week's core inflation numbers are hot again, the FOMC will need to consider tightening monetary policy soon.

By whichever measure you use, inflation has been rising this year.

Right now, I am concerned about the continued elevation in core inflation.

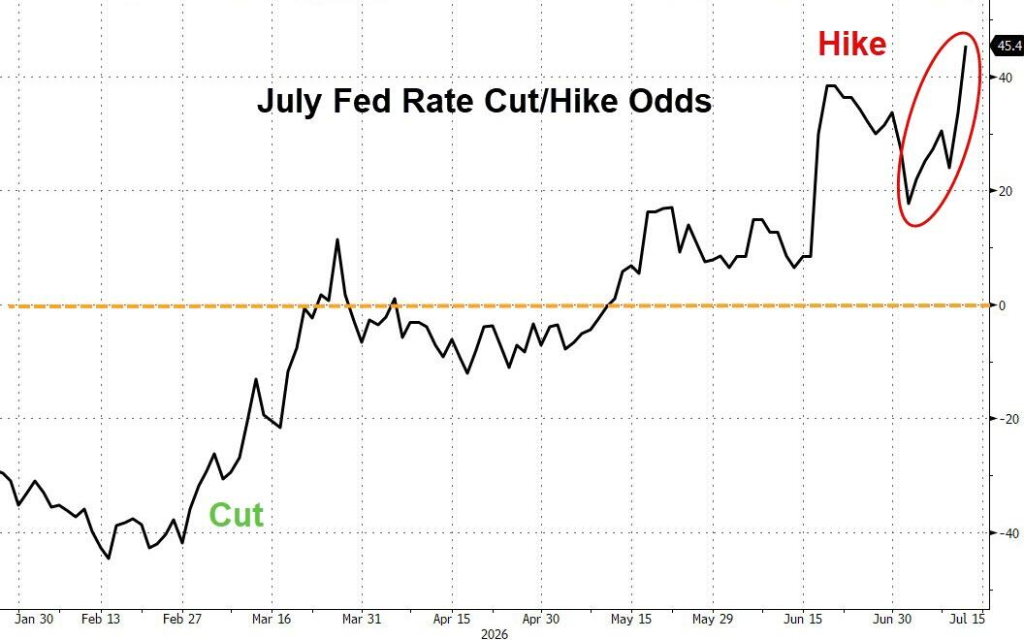

The 2-year US Treasury yield rose 6 basis points in a single day, the 30-year rose 3 basis points. The probability of a July rate hike surged to the highest since Waller took over, approaching 50%.

Krinsky from BTIG pointed out that the real yield on the 10-year Treasury has risen to its highest since April 2025, climbing from 2.11% at the end of June to 2.34%. His assessment:

If the real yield quickly breaks through 2.40%, it would be enough to cause a wider shock to the stock market.

Oil prices also added fuel to the fire. WTI climbed nearly 9% on the day, approaching $78, a new one-month high—as commercial transit through the Strait of Hormuz plunged to just 3 trips in 24 hours (compared with 57 at the June 24 rebound peak). Rising oil prices push up inflation expectations, further reinforcing the hawkish logic in the bond market.

What happens next?

Krinsky from BTIG outlines three possible scenarios and their probabilities:

- Rotation continues (40%): Funds keep flowing from semiconductors/tech/AI to other sectors

- Rotation reverses (20%): Funds flow back into tech, leaving recently strong sectors

- Rotation fizzles, broad selloff (40%): Correlations spike, market falls sharply, similar to late July 2024

Krinsky specifically noted that the probability of the third scenario "has risen sharply today"—due to the real yield surge, the overnight collapse of KOSPI, and the nearly 50% chance of a July rate hike.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

PBOC sets USD/CNY reference rate at 6.7990 vs. 6.7972 previous

Euro posts modest gains above 1.1350 as traders await US CPI inflation release

Bitcoin mining activity rises in Ethiopia as country becomes unlikely crypto powerhouse

Jito price recovers – Assessing if JTO can flip $0.67 into support