Bitget UEX Daily | US Media Reports US-Iran Ceasefire; South Korea Chip Giants Announce Trillion-Dollar Investment Plan; AI Application Software Sector Rises Sharply

2026/06/29 01:26

2026/06/29 01:26

一、Hot News

Federal Reserve Dynamics Gavekal: Scenario of Trump Pressuring the Fed into High Inflation Unlikely

- The firm noted that Kevin Walsh’s appointment as Fed Chair, along with the reappointment of 11 regional Fed presidents, has significantly reduced market concerns over the erosion of monetary policy independence. The Fed’s emphasis on price stability at its early June meeting surprised market participants who had anticipated a more dovish stance.

- The report stressed that while markets in 2025 feared Trump might appoint a political figure to force rate cuts and push inflation above target, developments over the past seven months have made this scenario significantly less probable.

- Market Impact: This view supports stability in the US dollar and Treasury yields, reduces tail-risk premiums, and provides a neutral-to-positive backdrop for risk assets.

International Commodities US and Iran Agree to Halt Mutual Attacks; Qatar Meeting in Doha This Week to Focus on Hormuz Strait

- According to Axios, a senior US official confirmed that the US and Iran have agreed to cease all military actions, with a meeting scheduled for Tuesday in Doha, Qatar, to resolve disputes over the Strait of Hormuz. Previously, on June 27, President Trump warned that if Iran violated the ceasefire again, the US might resume military action to “finish the job,” stating that the Islamic Republic of Iran could cease to exist.

- Iranian Foreign Minister Araghchi stated that the Strait of Hormuz would remain under full Iranian supervision and management for the next 30 days. Technical talks originally planned in Switzerland have stalled due to recent clashes, and Iranian officials were absent from negotiations on the 28th.

- Market Impact: The de-escalation signal is clearly positive for risk assets. Oil prices face downward pressure, while safe-haven demand for gold and other assets fluctuates in the short term, though overall risk appetite has improved.

Stock Market South Korea Announces “Three Major Projects” Investment Plan Today; Scale May Exceed $650 Billion

- President Lee Jae-myung will deliver a speech this afternoon at the Blue House. Four government ministries, including the Ministry of Trade, Industry and Energy, will simultaneously release policy and investment announcements. Samsung Electronics and SK are expected to unveil corporate investment plans totaling over 1,000 trillion KRW (approximately $650 billion) over the next decade, potentially including the development of a semiconductor cluster in the southwestern Honam region.

- President Lee described the move as a “historic achievement” aimed at strengthening South Korea’s position in the global AI chip supply chain.

- Market Impact: Global semiconductor and AI infrastructure supply chain assets are expected to receive long-term catalysts, benefiting US tech stocks and related ETF flows.

二、Market Review

Commodities & Forex Performance (Real-time Update)

- Spot Gold: ~$4,056/oz, -0.76%

- Spot Silver: ~$58.9/oz, -1.38%

- WTI Crude: ~$70.1/barrel, +1.4%

- Brent Crude: ~$73.4/barrel, +1.2%

- US Dollar Index (DXY): ~101.34, -0.03%

Driver Analysis: The agreement between the US and Iran to halt mutual attacks and shift discussions to a meeting in Doha has improved the outlook for the reopening of the Strait of Hormuz, directly easing supply concerns in the oil market. Both WTI and Brent are under pressure. Gold and silver saw modest gains amid improved risk appetite and confirmation of Fed policy independence. The dollar index edged lower. Institutions believe that while geopolitical easing is positive for risk assets, inflation concerns and the Fed’s stance continue to provide support for precious metals. In the short term, oil prices are more likely to fall than rise, while precious metals are expected to trade in a range with a slight upward bias. The inter-asset linkage is clear: lower oil prices → reduced inflation pressure → slightly higher rate-cut expectations → weaker dollar → support for gold.

Cryptocurrency Performance

- BTC: ~$59,575, -1%

- ETH: ~$1,570, -0.31%

- Total Crypto Market Cap: ~$2.13 trillion, -1.2%

- Market Liquidations (24h): Total ~$184 million, of which long liquidations accounted for ~$148 million

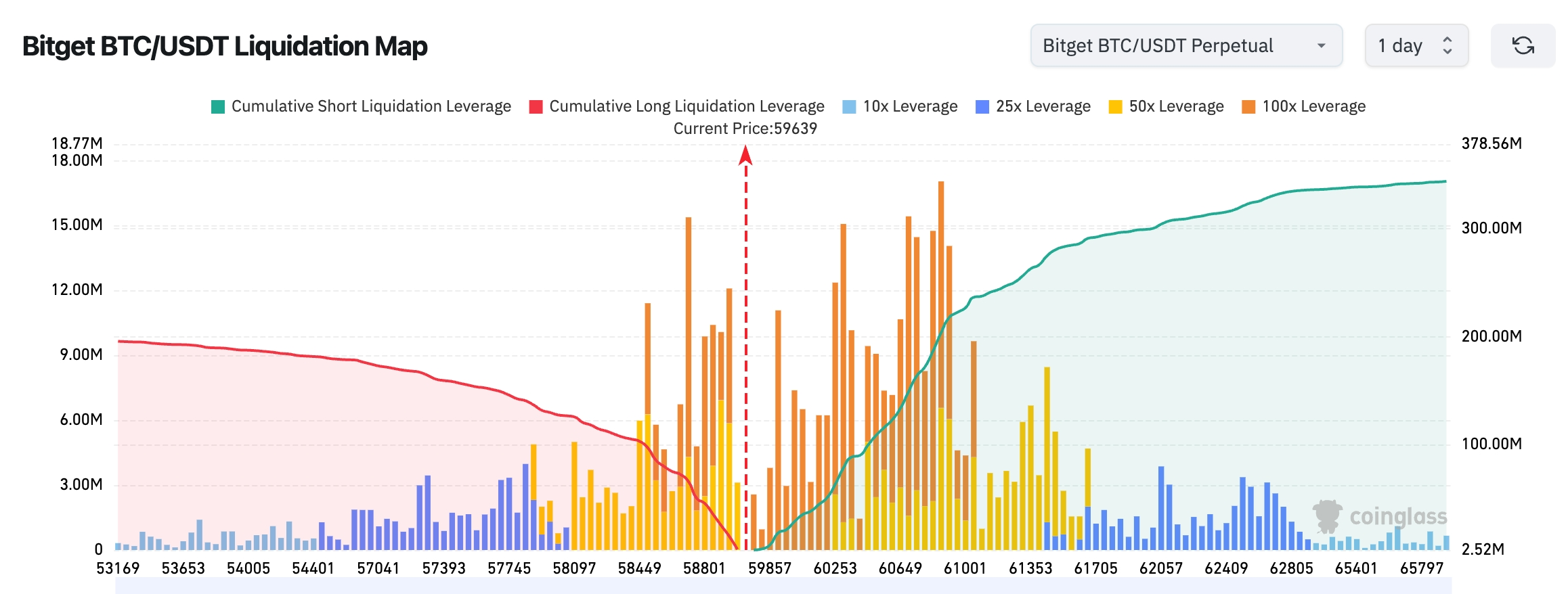

- Bitget BTC/USDT Liquidation Map: BTC is currently trading around $59,639. A large cluster of short liquidation levels is concentrated in the $60,200–61,000 zone. A decisive break above the $60,000 psychological level could trigger a short squeeze and further upside. On the downside, long liquidation clusters are mainly located between $58,000–59,000, with significantly smaller total volume compared to the upside. Overall, the map shows denser liquidity above current prices, suggesting a short-term structural bias toward attracting upside liquidity.

- Spot ETF Net Flow: On Friday’s close, BTC spot ETFs recorded a single-day net outflow of approximately $445 million.

Driver Analysis: Geopolitical easing has boosted overall risk appetite, but the affirmation of Fed independence by institutions and persistent ETF outflows since June have prevented BTC from staging a strong rebound. Leverage liquidation volumes have declined sharply from previous levels, indicating that highly leveraged positions have been largely flushed out and the market has entered a low-volatility repair phase. Technically, the $59,300 area remains a key battleground between bulls and bears. The dense short cluster above could act as near-term resistance, while a break below the $58,000 support may trigger further cascading liquidations. The broader trend still requires confirmation from ETF flows and upcoming macroeconomic data.

US Stock Index Performance

- Dow Jones: 51,876.11 points (-0.09%)

- S&P 500: 7,354.02 points (-0.05%)

- Nasdaq: 25,297.62 points (-0.24%)

Tech Giants Performance

- NVDA: $192.53, -1.64%

- AAPL: $283.78, +3.14%

- MSFT: $372.97, +5.71%

- GOOGL: $337.39, -1.84%

- AMZN: $232.69, +2.50%

- META: $550.25, +1.36%

- TSLA: $379.71, +1.22%

- MU: $1,132.33, -6.69%

- SPCX: $153.23, +0.15%

Performance Summary & Driver Analysis: The tech sector showed clear divergence on Friday, driven by stock-specific factors rather than a single macro theme. Heavyweights such as MSFT, AAPL, and AMZN posted strong gains, supported by robust AI cloud demand and company-specific positive developments. In contrast, semiconductor names including NVDA and MU (-6.69%) declined due to profit-taking and concerns over supply dynamics and competition. While geopolitical easing lifted overall risk sentiment, internal competition and valuation pressures within the chip sector remained the dominant drivers. A “one-size-fits-all” explanation should be avoided. This divergence is expected to persist in the near term, with AI application and infrastructure leaders showing relative resilience.

Crypto-Related Stock Contracts Overview

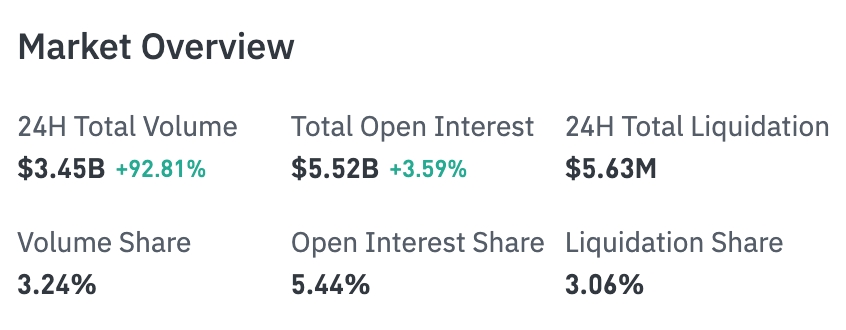

- 24H Total Trading Volume: $3.441 billion (+92.31%)

- Open Interest (OI): $5.523 billion (+3.68%)

- 24H Total Liquidations: $5.6186 million

- Volume Share: 3.23%

- OI Share: 5.44%

- Liquidation Share: 3.05%

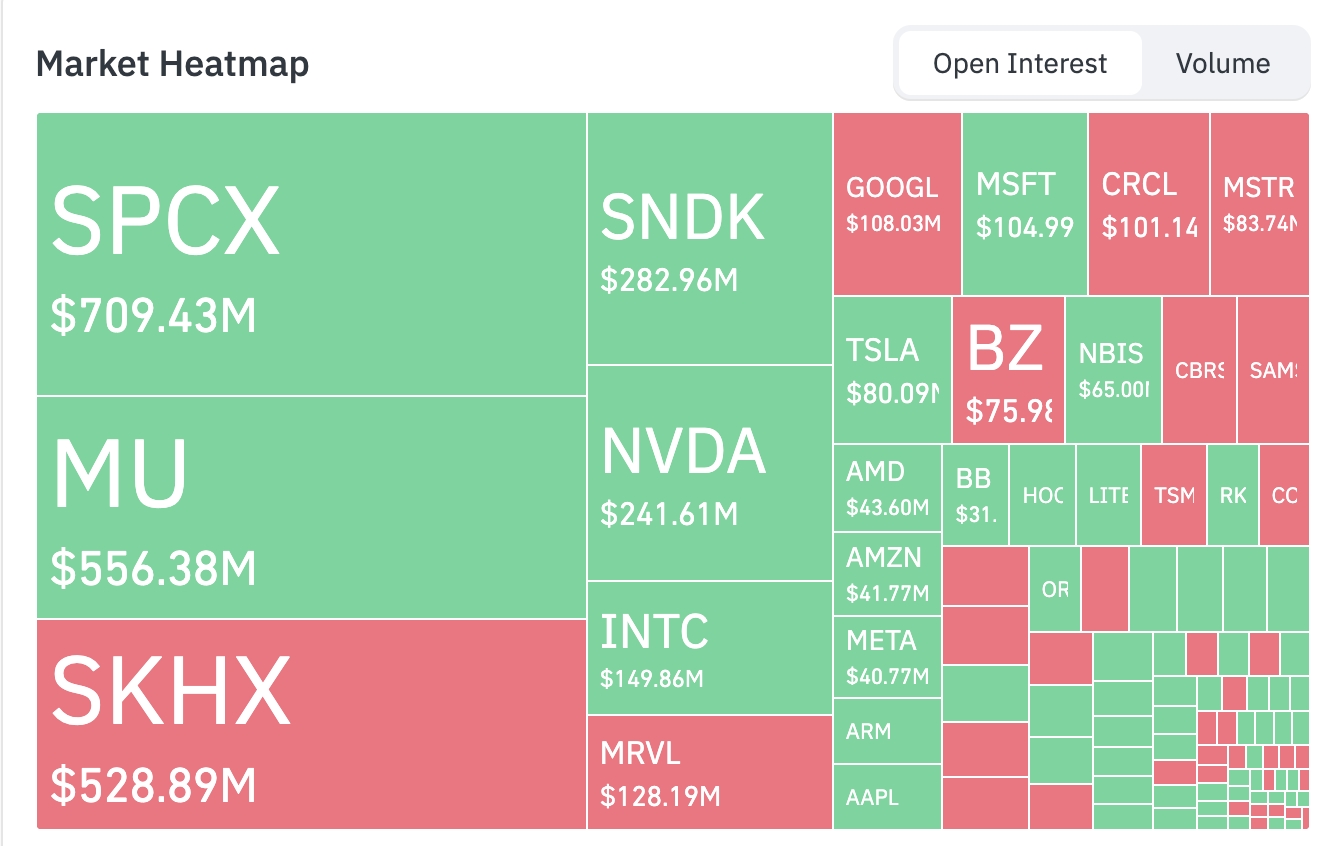

Position Heatmap Highlights

SPCX: $710 million | MU: $556 million | SKHX: $530 million | SNDK: $283 million | NVDA: $242 million | INTC: $150 million | MRVL: $129 million | GOOGL: $108 million | MSFT: $105 million | CRCL: $101 million

Sector Rotation Observation

Semiconductor Sector fell more than 5%

- Representative stocks: MU -6.69%, AMD -2%, NVDA -1.64%

- Drivers: Profit-taking intensified on Friday, compounded by market concerns over potential AI chip oversupply and intensifying competition. The Philadelphia Semiconductor Index declined in tandem.

AI Application Software Sector rose sharply (some stocks up 8–10%)

- Representative stocks: NOW and SNOW up nearly 10%, WDAY +9%, DDOG +8%

- Drivers: Continued enterprise adoption of AI, sustained strong demand for cloud services and data analytics. Capital rotated back into high-growth segments after recent pullbacks.

Crypto Concept Stocks mostly advanced

- Representative stocks: HOOD +6%, COIN and HUT +4%

- Drivers: Geopolitical easing improved risk appetite. Cathie Wood’s ARK funds made significant purchases of COIN and other names, boosting sentiment in the sector.

三、In-Depth US Stock Analysis

1. Microsoft – AI Cloud Demand Drives Strong Friday Gains Event Overview: MSFT rose approximately 5.71% on Friday, significantly outperforming the broader market. The move was primarily driven by continued strong demand for AI-related cloud services and enterprise solutions. The market interpreted this as confirmation that the AI capex cycle remains in an acceleration phase and that Azure’s growth outlook has been further validated. Market View: Institutions generally believe Microsoft’s dual positioning in AI infrastructure and applications gives it both defensive and offensive characteristics in the current environment. Buying interest has strengthened following the recent pullback. Investment Insight: Short-term focus should be on upcoming Azure AI metrics. The stock remains a core long-term holding in the technology sector.

2. Micron (MU) – Semiconductor Cycle Volatility Triggers Sharp Pullback Event Overview: MU fell nearly 7% on Friday, weighing on the broader semiconductor sector. The decline was attributed to profit-taking after strong prior gains and growing concerns about the timing of AI chip supply relative to downstream demand. Market View: Institutional opinions are divided. Some view the move as a healthy correction, noting that long-term HBM and memory demand remains supportive. Others caution that near-term inventory and pricing pressures warrant attention. Investment Insight: Suitable for high-risk investors to accumulate near support levels with strict stop-loss discipline.

3. Coinbase (COIN) – ARK Invest’s Large Purchase Boosts Market Confidence Event Overview: On June 26, Cathie Wood’s ARK Invest spent approximately $10.19 million to purchase COIN shares, while also adding to positions in SpaceX and Circle. Market View: The move is seen as a vote of confidence from a well-known growth investor in crypto infrastructure and compliant platforms, carrying signaling value amid ongoing ETF outflows. Investment Insight: Short-term, it can serve as a sentiment indicator. Longer-term, regulatory developments and actual adoption rates remain key to monitor.

四、Views & Market Dynamics

- US House Speaker Mike Johnson stated that a housing bill containing a temporary ban on CBDCs (until 2030) will be sent to President Trump on Monday for signing into law. Earlier reports on June 24 indicated that Trump had refused to sign a previous version containing the CBDC ban, pushing instead for election-related legislation.

- Arthur Hayes posted on X that he remains bullish on the Hyperliquid ecosystem but is looking for more asymmetric opportunities. He suggested it is time for an options DEX to genuinely challenge Deribit, and that Hypercall (SYN) could be such a contender. He previously purchased 6.16 million SYN tokens from FlowDesk for approximately $2.2 million.

- A senior US official said the United States and Iran have agreed to stop mutual attacks and plan to meet in Doha, Qatar, on Tuesday to resolve disputes regarding the Strait of Hormuz. Previously, just 11 days after the ceasefire memorandum was signed, both sides launched attacks again, and President Trump threatened to restart the war and “finish the job.”

- Bitcoin advocate Samson Mow stated on social media that he believes the bottom of the current Bitcoin cycle has formed. He noted that the traditional “four-year halving cycle” appears to be breaking down, with market rhythms accelerating. He highlighted that Bitcoin reached an all-time high 37 days before the April 2024 halving, suggesting cycle dynamics are speeding up. While he acknowledges the reference value of cycle models, he believes their effectiveness should be reassessed. With continuous institutional inflows via spot ETFs, Bitcoin’s market structure has changed, and traditional methods of identifying tops and bottoms based on historical halving cycles are losing relevance. He views the current price range as having characteristics of a cycle bottom. However, market views remain divided. 10x Research founder Markus Thielen believes the bottom is more likely around $55,000, possibly between August and October. BitMEX co-founder Arthur Hayes expects Bitcoin could drop to around $40,000 in the coming months. CoinDesk analyst James Van Straten noted that based on long-term indicators such as the 200-week moving average, Bitcoin may still need to fall another 15% or more to complete the final bottoming process, with the $50,000–$54,000 zone potentially becoming a key battleground.

- Framework Ventures co-founder Michael Anderson stated that the next phase of opportunity in crypto may no longer be limited to crypto assets themselves, but rather in becoming the financing infrastructure for capital-intensive industries such as artificial intelligence, robotics, and energy. Tokenization and stablecoins are evolving from crypto-native applications into financial infrastructure serving the real economy, usable for more efficient financing of GPU compute, energy projects, and other real-world assets. Compared with the 2020–2021 cycle centered on DeFi and crypto speculation, the industry is shifting toward “real-world financing and infrastructure development.” Blockchain is upgrading from a transactional application layer to a cross-industry capital network. He emphasized that the current stage may mark a structural shift in crypto from “speculation-driven” to “infrastructure-driven.”

五、Today’s Market Calendar

Important Events

- South Korea Chip Investment Plan Release: This afternoon — Focus on specific investment scale and regional layout details for Samsung and SK.

Institutional Views: Against the backdrop of US-Iran de-escalation, South Korea’s major investment plan announcement, and institutional affirmation of Fed independence, most investment banks and research institutions believe the near-term environment for risk assets has improved marginally. The cooling of geopolitical tensions is directly positive for lower oil prices and improved equity risk appetite. South Korea’s trillion-dollar-scale chip investment provides long-term support for the global semiconductor and AI supply chain. Stable expectations regarding Fed policy independence have reduced tail risks of extreme inflation or policy missteps, supporting the dollar and Treasuries. However, the crypto market still faces pressure from ongoing ETF outflows and post-liquidation confidence repair, with BTC likely to remain range-bound in the near term. Overall, institutions remain optimistic about US tech leaders and the semiconductor supply chain over the medium to long term, maintain a neutral-to-bullish stance on precious metals, and recommend cautious positioning in crypto while monitoring the $59,000 key support level. Short-term trading strategies should closely track marginal changes in geopolitics and macroeconomic data while controlling position size and leverage.

Disclaimer: The above content is compiled by AI and verified by humans before publication. It does not constitute any investment advice. Data in this report may contain inaccuracies; please refer to real-time market data for the most accurate information.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

PBOC sets USD/CNY reference rate at 6.7990 vs. 6.7972 previous

Euro posts modest gains above 1.1350 as traders await US CPI inflation release

Bitcoin mining activity rises in Ethiopia as country becomes unlikely crypto powerhouse

Jito price recovers – Assessing if JTO can flip $0.67 into support